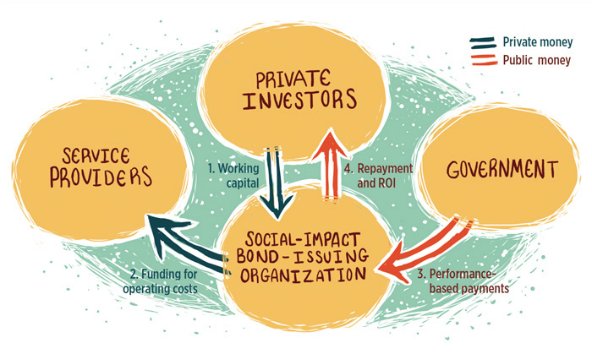

At first glance, social impact bonds (SIBs) appear to be an ideology-free response to a range of social problems. As public resources are not always made available to adequately fund public and social services, SIBs leverage private investment to finance such services so that providers do not have to front the cost of delivery. Investors are rewarded if providers meet agreed-upon outcomes but lose their investment if providers do not meet those outcomes. On the face of it, SIBs might seem like a win-win for everyone involved.

So it makes some sense that SIBs have become so popular. Since their introduction in 2010, 32 SIBs have been set up thus far in the United Kingdom, addressing diverse policy areas such as homelessness, mental health services, education, and unemployment. The UK Government Cabinet Office has established a Centre for Social Impact Bonds. The government also allocated more than $28 million of public funding to a Social Outcomes Fund in 2012 for the development of SIBs, and augmented this by a further $113.4 million from the UK Government’s Life Chances Fund in 2016—significant amounts of money by any measure. The UK’s Minister for Civil Society has said that SIBs will revolutionize the third sector and social service funding, and that a SIBs market in Britain could be worth $1.4 billion by 2020. Meanwhile, there are at least 10 SIBs operating in the United States and 19 more across 14 other countries, with Goldman Sachs also investing in the model. The development community has also adapted the SIB model in service of so-called development impact bonds (DIBs), primarily for use in the global south.

Please continue to the full article on SSIR.

Leave A Comment